WAYS TO INVEST: REGULAR PAYMENTS OR LUMP SUM?

Many people are put off investing because they assume they need a large lump sum of money to invest. But it is possible, and sometimes preferable, to invest by making regular payments of as little as GH¢50 into a fund.

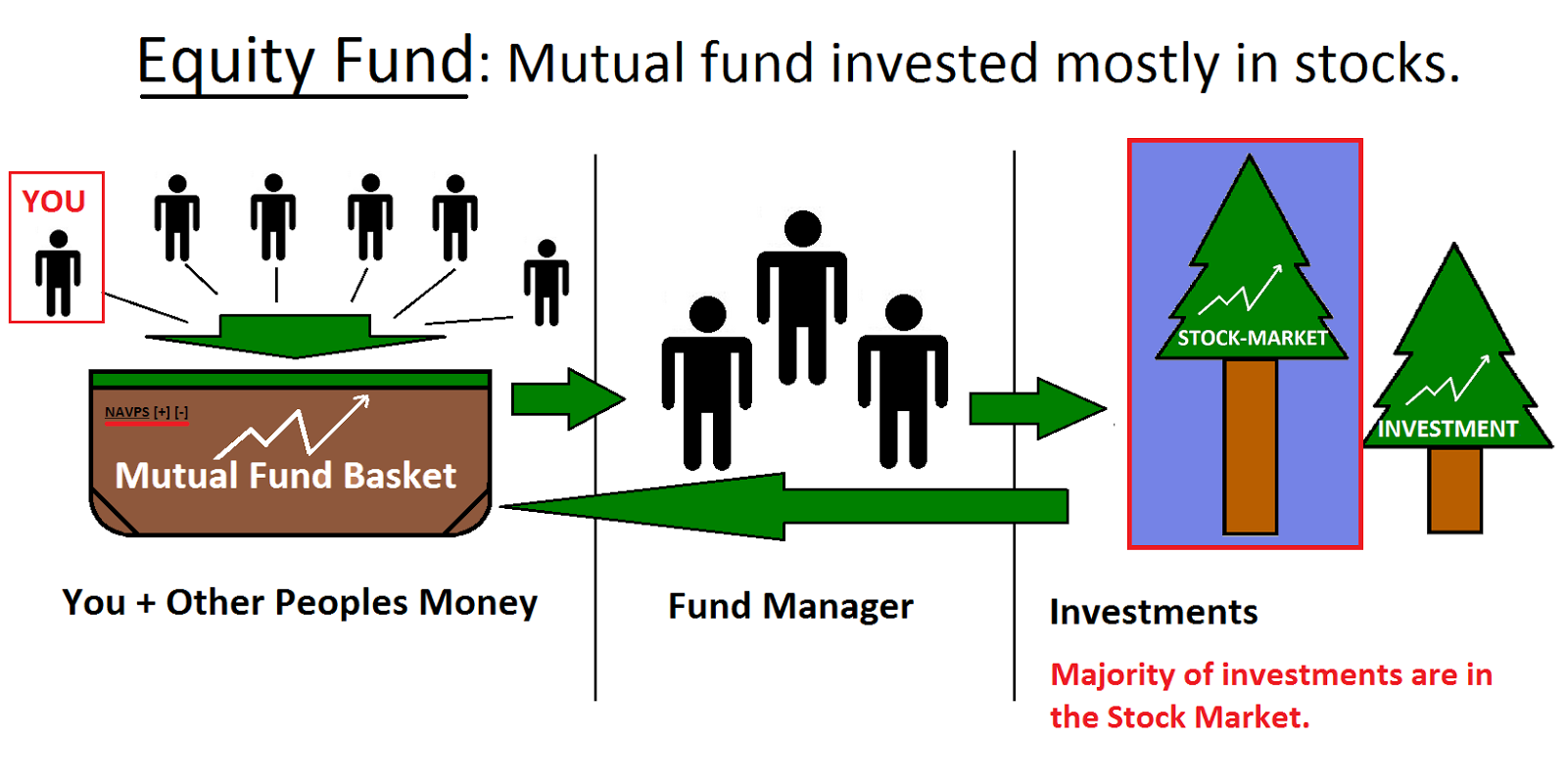

How Monthly Payments Help

Regular payments into an equity fund are not only easier for most people, they can benefit from the ‘cedi cost averaging’ effect. Because stock market prices may be up one month and down the next, monthly payments mean that you’ll pay an average price during the course of the year.

You can also gain a better picture of the market, which means you are less likely to invest in shares which are actually rising only temporarily before sharply falling again. Regular payments can also be less risky than lump sum investments: if the market collapses, payments can be stopped.

However, the more you invest and the longer you invest for, the greater the potential return. So if you can afford to invest a lump sum at a time when the market is rising, you have a distinct advantage over a regular payment investor.

Lump Sum Investment: How to Spread the Risk

Getting a large amount of money out of the blue can be quite overwhelming, and it can be tempting to rush out and spend it all on frivolous things which depreciate as soon as they leave the shop. If you’re lucky enough to receive a windfall, putting it away in a high interest savings account and ‘sleeping on it’ until you decide what you really want to do with it, can often save regrets later.

Before investing your money, consider paying off any debts you may have. Provided that the interest you pay on loans is more than the returns you could earn from your investments, this makes clear financial sense. As well as leaving you with more disposable income, getting rid of debts is usually a weight off your mind.

Spreading your money across different products of varying degrees of risk generally gives you the best chance of making your money grow, while retaining a measure of security.